Year-End Corporate Tax Planning Guide: 2025 Tax Efficiency Strategies for UK Businesses

Year-End Corporate Tax Planning Guide 2025: Master capital allowances, profit extraction strategies, R&D relief, and deadline management to minimize tax and maximize profits.

FINANCE

Rudra Prakash Parida

12/8/202514 min read

Year-End Corporate Tax Planning Visual Guide

Year-End Tax Planning: 2025 Snapshot

Who this guide is for: UK limited-company owners, FDs, and finance leads with profits between £50,000–£500,000.

Main goals: Reduce 2025 corporation tax, optimise profit extraction, and avoid deadline penalties.

Key levers: Capital allowances, profit-extraction mix (salary/bonus/dividend/pension), loss relief, R&D claims, and charitable giving.

Urgent dates to act by:

Financial review by 15 December

Investment & giving decisions by 20 December

Profit extraction decisions by 28 December

Documentation & compliance by 31 December

Estimated impact: Well-executed planning can save tens of thousands of pounds over time for growing companies.

2025 Tax Efficiency Strategies for UK Businesses

Effective year-end corporate tax planning is one of the most powerful tools available to UK business owners. With proper strategy, companies can significantly reduce their corporation tax liability, optimize profit extraction, and position themselves for stronger financial performance in the coming year. This comprehensive guide explores the essential tax planning strategies, deadlines, and opportunities you need to maximize tax efficiency before December 31st.

Understanding the 2025 UK Corporation Tax Landscape

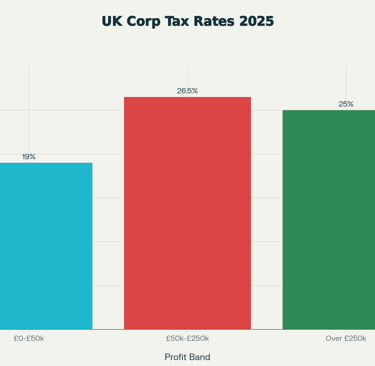

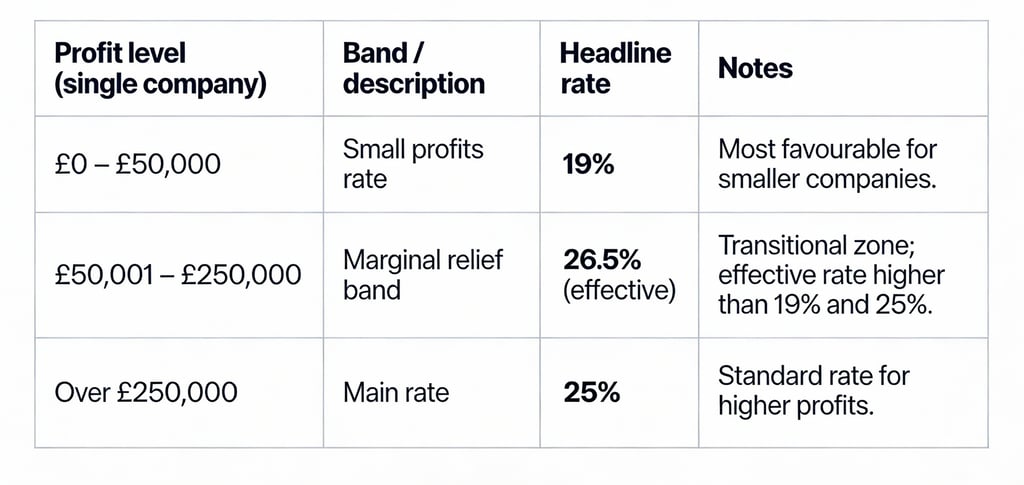

The UK corporation tax system operates on a banded structure that rewards smaller profits while maintaining higher rates for larger earners. For 2025/26, the framework remains consistent but understanding how these bands function is critical for strategic planning.

UK businesses are subject to a tiered corporation tax system with three distinct profit brackets. Companies earning profits between £0 and £50,000 benefit from the small profits rate of 19%, making this the most favorable bracket for smaller enterprises. The transition zone between £50,001 and £250,000 is where marginal relief applies, creating an effective tax rate of 26.5% during this period. Finally, companies exceeding £250,000 in profits fall into the main rate of 25%.

December 2025 Action Timeline

By 15 December – Financial Review

Project year-end profit; identify small profits, marginal, or main rate band.

Review three-year loss position and carried-forward losses.

By 20 December – Investment & Giving

Audit capital expenditure; check AIA and potential accelerated purchases before April 2026.

Decide on any charitable donations and Gift Aid planning.

By 28 December – Profit Extraction

Model dividend vs bonus vs pension contribution scenarios.

Decide salary/dividend/bonus/pension mix for directors.

By 31 December – Documentation & Compliance

Finalise records, document decisions, and prepare for CT deadlines (9 months + 1 day; 12 months for CT600).

The significance of these bands cannot be overstated. A company earning £49,000 pays just £9,310 in corporation tax, while a company earning £50,000 faces £13,250 a jump of nearly £4,000 on just £1,000 more profit. Understanding where your business falls within these brackets is the foundation of effective tax planning, as it informs which strategies will deliver the greatest benefit.

Action Point: Calculate your projected year-end profit position now. This determines which tax planning strategies will be most beneficial for your situation.

Critical Year-End Tax Planning Deadlines

One of the most overlooked aspect of year-end tax planning is managing multiple regulatory deadlines. Missing these dates can result in unnecessary tax payments, penalties, and lost opportunities.

The most fundamental deadline is understanding your company's accounting year-end. While 31 December is common, many businesses operate on different accounting periods such as 31 March or 30 June. Corporation tax payments are typically due nine months and one day after your accounting year-end. This means a December year-end company must pay by 30 September, while a March year-end company has until 1 January.

The corporation tax return itself must be filed within 12 months of your accounting period end. Failure to meet this deadline triggers automatic penalties that can reach 100% of the unpaid tax in cases of prolonged non-compliance. These deadlines are non-negotiable—HMRC applies penalties systematically.

Beyond corporation tax deadlines, if your company operates on a calendar year-end, you have just weeks to implement remaining tax strategies before December 31st. This creates genuine urgency for planning and execution.

Critical Action Items:

Confirm your company's accounting year-end and mark the tax payment deadline (9 months + 1 day)

Schedule your corporation tax return submission (12 months from year-end)

For December year-ends: implement strategies before 31 December 2025

Document all year-end decisions with clear audit trails

Maximizing Capital Allowances and Plant & Machinery Relief

Capital allowances represent one of the most generous and underutilized tax reliefs available to UK businesses. These provisions allow you to deduct the cost of capital assets against profits, reducing your corporation tax liability dollar-for-dollar.

The Annual Investment Allowance (AIA) provides 100% tax relief on qualifying equipment investments up to £1 million per year. This means if your company purchases £100,000 worth of qualifying plant or machinery, you can claim a full £100,000 deduction against profits in that year, saving up to £25,000 in corporation tax (at the 25% rate).

However, significant changes are coming to capital allowance rules in 2026. The government is reducing the main rate of Writing-Down Allowance (WDA) from 18% to 14% per year, effective from 1 April 2026. This reduction presents a compelling case for accelerating qualifying purchases before the new rates take effect. Assets purchased before April 2026 will continue to benefit from the more generous 18% WDA rate, while new purchases will be subject to the lower 14% rate indefinitely.

Simultaneously, the government is introducing a new 40% First-Year Allowance (FYA) for main rate assets, effective from 1 January 2026. This provides accelerated relief for plant and machinery, though it excludes second-hand assets, cars, and assets for overseas leasing. For qualifying new equipment, this represents a significant tax benefit.

Equipment that qualifies includes: machinery, plant, fixtures, IT equipment, and manufacturing equipment. Equipment that does not qualify includes: buildings, land, integral parts of buildings (electrical systems, plumbing), and motor vehicles for private use.

Strategic Consideration: If you're planning significant capital investment, timing the purchase before April 2026 could yield substantial tax savings. Conversely, if your business doesn't have immediate investment needs, the new 40% FYA may make future purchases more tax-efficient.

Profit Extraction: Dividend vs. Bonus Strategy for 2025/26

One of the most significant year-end decisions for business owners is choosing between extracting profits as dividends or bonuses. This choice has profound implications for your personal tax liability and your company's tax position. The optimal strategy has shifted with recent changes to tax rates.

For most of this decade, dividend extraction was substantially more tax-efficient than bonus extraction. However, the 2025 Autumn Budget changed personal income tax rates, fundamentally altering the mathematics. As of April 2026, the ordinary dividend allowance increases from 8.75% to 10.75%, while the higher rate increases from 33.75% to 35.75%.

For a company paying corporation tax at 19% (small profits rate), dividend extraction generally remains the more tax-efficient option, with an effective rate of approximately 25% for basic rate taxpayers versus 29.4% for bonus extraction. However, for companies paying the main corporation tax rate of 25%, the picture reverses: bonus extraction becomes slightly more efficient at 29.4% versus 30.4% for dividend extraction for basic rate taxpayers.

For higher rate taxpayers, the differential becomes even more pronounced. At the 25% corporation tax rate, bonus extraction at 48.3% is significantly more efficient than dividend extraction at 51.8%.

The practical implication: larger companies with higher corporation tax rates should seriously evaluate bonus extraction as their primary profit-extraction mechanism, even though bonuses require PAYE processing and National Insurance contributions.

Action Items:

Model both dividend and bonus scenarios for your business

Calculate your personal marginal tax rate and your company's corporation tax rate

Consider whether bonus extraction aligns with your salary pattern and employer's NI position

Document the decision before implementing profit extraction

Profit Extraction: Quick View (2025/26)

For companies at 19% CT: dividends often more efficient for basic rate owners.

For companies at 25% CT: bonuses can become more efficient, especially at higher personal tax bands.

Pension contributions usually win on pure tax efficiency but reduce short-term cash access.

Best results often come from a blended mix of salary, bonus, dividend, and pension.

Leveraging Trading Losses and Loss Relief Mechanisms

Trading losses represent valuable assets that many business owners inadvertently waste. When your company generates a loss in an accounting period, multiple relief mechanisms allow you to recover this value through corporation tax reduction.

Trading losses can be carried forward indefinitely to offset against future profits in subsequent accounting periods, providing long-term tax relief. However, specific limitations apply to carried-forward losses, particularly those arising before 1 April 2017. For older losses, relief is restricted to £5 million plus 50% of remaining profits.

For losses arising after 1 April 2017, the restriction is more generous but still applies: you can offset losses against profits up to £5 million, with 50% relief on profits exceeding this threshold. This means a company with £10 million in profits can use carried-forward losses to offset the first £5 million (£5 million allowance) plus 50% of the remaining £5 million (£2.5 million), totaling £7.5 million in loss relief.

Immediate loss relief options also exist if you have other sources of profit within your company. If your limited company also generates capital gains, certain types of losses can be offset against those gains in the same accounting period. Additionally, if your company operates multiple trades or has rental income, trading losses can provide relief across these activities.

Group relief represents another powerful mechanism for multi-company structures. If your company is part of a corporate group, trading losses can be surrendered to another group company to offset its taxable profits, subject to specific rules about group membership and loss ownership.

Strategic Action: Review the past three years of your company's profit and loss statement. If any losses were generated and not fully utilized, explore whether carried-forward relief, group relief, or immediate offset opportunities remain available.

Pension Contributions: Tax-Efficient Profit Extraction

Pension contributions represent the most tax-efficient mechanism available for extracting profits from your company while simultaneously building retirement security. Unlike dividends or bonuses, pension contributions deliver comprehensive tax relief across multiple tax layers.

Employer pension contributions are fully allowable business expenses, meaning your company receives a deduction against taxable profits at the corporation tax rate. If your company is in the 25% bracket, a £10,000 pension contribution reduces corporation tax by £2,500.

As a company director, you can personally contribute up to £60,000 per tax year into your pension (known as the "Annual Allowance"), as long as your company has sufficient profits to support this contribution. The entire contribution is made with corporation tax relief, and you personally avoid both income tax and National Insurance on the amount contributed.

The mechanics are straightforward: your company makes a contribution to a pension scheme in your name, the contribution is deducted from company profits, and you receive no personal income tax charge. This differs from salary-related pension contributions, where the contribution is subject to PAYE deductions.

Critical limitation: The contribution must pass the "wholly and exclusively" test, meaning it must be made wholly and exclusively for the purposes of the employer's trade or profession. In practice, this means the contribution must genuinely be a business decision rather than a personal savings mechanism.

For directors with limited profits, a more conservative contribution approach is prudent. If profits are uncertain, consider making a smaller contribution that doesn't jeopardize the business's cash position. Overcommitting to pension contributions and then having to unwind them creates accounting complexity and potential tax complications.

Planning Action: Calculate your available profit after all essential business expenses. If profits exceed £60,000, consider whether pension contributions could form part of your year-end tax planning, potentially combined with dividends or bonuses for the remainder.

Research and Development Tax Relief: Reclaiming Investment

If your company invests in research, development, or innovation even unsuccessful projects you may qualify for substantial corporation tax relief through the R&D Tax Credit scheme. This relief effectively reimburses companies for their investment in innovation.

Significant changes took effect from April 1, 2024 (for accounting periods ending March 31, 2025 and later). The scheme now operates through two distinct mechanisms depending on your company's circumstances.

For profitable companies, the new Research and Development Expenditure Credit (RDEC) offers tax relief of approximately 15p-16p in every £1 spent on qualifying R&D expenditure. This credit is applied above the tax line, meaning it reduces corporation tax liability after profits are calculated.

For loss-making, R&D-intensive companies (where R&D represents at least 30% of total expenditure), the enhanced R&D Intensive Support Scheme (ERIS) provides more generous relief of up to 27p in every £1 spent. This significantly higher rate reflects the government's commitment to supporting innovation in smaller and struggling businesses.

A major change in 2024 relates to grants and subsidies. Previously, companies receiving grants for R&D were restricted in how they could claim relief. Now, companies can claim under either the new RDEC or ERIS regardless of whether their R&D projects are grant-funded. This eliminates a previous administrative burden and expands relief availability.

Qualifying R&D expenditure includes staff costs, subcontracted research, materials, and software licenses used in qualifying research activities. Non-qualifying expenses include acquired assets, general business operating costs, and routine testing or quality assurance.

Documentation requirement: R&D relief requires detailed contemporaneous documentation of the research activities undertaken, the methodologies tested, and why the project constituted genuine R&D. Companies should maintain project notes, emails discussing problems encountered, and technical decision records.

Action Point: If your company has undertaken any research, development, or innovation activities in the past three years, review whether you've claimed all available R&D relief. Many companies leave thousands of pounds unclaimed annually.

Charitable Donations and Gift Aid Tax Relief

Corporate charitable giving combines social impact with legitimate tax deductions. Unlike many tax planning strategies, charitable donations deliver immediate tax relief while supporting causes aligned with your business values.

Qualifying charitable donations are fully deductible from corporation tax if the recipient is a UK registered charity and there is no direct business benefit to the donor. A £10,000 donation to a qualifying charity reduces corporation tax by £2,500 (at 25% rate), effectively costing your company only £7,500 of after-tax profit.

Gift Aid mechanism further enhances the relief available. When a charity receives a donation with Gift Aid declared, the charity can claim an additional 25% from HMRC. If your company donates £1,000 with Gift Aid, the charity receives £1,250, with HMRC contributing the additional £250.

Critical requirement: The donation must be made in genuine charitable intent with no expectation of return benefit. If your company receives corporate hospitality, advertising, or other benefits from the charity, the donation may not qualify for relief. The key test is whether the donation creates a "quid pro quo" arrangement.

For strategic giving, consider whether December gifts deliver additional year-end tax efficiency. If your company is positioned just above a profit threshold (such as £250,000 separating the 25% and 19% rates), a well-timed charitable donation could push profits below the threshold, triggering marginal relief.

Timing consideration: Donations made by December 31 must be recorded in that year's accounts and tax position, so documentation must be complete before year-end.

Additional Tax Planning Strategies: Marginal Relief and Loss Structuring

The marginal relief system creates specific opportunities for companies positioned between profit bands. If your company's profits fall in the £50,000-£250,000 range, marginal relief applies a tapered effective rate of 26.5%, creating a higher rate than both lower and higher profit brackets.

For companies approaching the £250,000 threshold, strategic expense acceleration becomes valuable. Accelerating deductible expenses from January to December effectively reduces current-year taxable profits, potentially dropping below the £250,000 bracket. This reduces both current-year corporation tax and addresses the threshold for associated companies (where multiple group entities share limits).

Associated company rules limit the profit threshold for related entities. If your business operates multiple limited companies (perhaps separate legal entities for different ventures), each entity shares a single £50,000 and £250,000 threshold across the entire group. Strategic structuring can optimize how profits and thresholds are distributed.

Loss utilization strategies for multi-company structures deserve careful attention. Group loss relief allows one company to surrender losses to another group company in the same accounting period. For integrated business operations with one profitable entity and one loss-making entity, this mechanism effectively consolidates the group's tax position.

Practical Year-End Tax Planning Checklist

Implementing a comprehensive year-end tax strategy requires systematic execution across multiple dimensions. Use this checklist to ensure no opportunities are overlooked.

Financial Review (By December 15):

Calculate projected year-end profit position

Identify whether profit will fall within small profits rate (under £50,000), marginal relief band (£50,000-£250,000), or main rate (over £250,000)

Review three-year loss position and carried-forward losses

Analyze whether any trading losses remain unclaimed from prior years

Identify available associated company threshold allocation if operating group structure

Calculate projected corporation tax liability under current profit trajectory

Capital and Investment Planning (By December 20):

Audit capital expenditure plans; identify qualifying plant and machinery

Calculate AIA availability (up to £1 million per year)

Consider accelerating qualifying purchases before April 2026 (before WDA rates reduce from 18% to 14%)

Review existing capital allowances claims to ensure no assets were overlooked

Evaluate whether new 40% FYA (from January 2026) should influence timing of purchases

Profit Extraction and Remuneration (By December 28):

Model dividend vs. bonus scenarios under 2025 tax rates

If using bonus extraction, ensure sufficient profit reserves and consider PAYE implications

If using dividend extraction, verify retained profit availability and document dividend resolution

Calculate pension contribution strategy; model £0, £30,000, and £60,000 scenarios

Determine optimal combination of salary, pension, dividend, and bonus

Charitable and Corporate Giving (By December 20):

Identify potential charitable recipients aligned with business values

Calculate Gift Aid declarations to maximize charity benefit

Consider charitable donation as marginal relief optimization tool if near profit thresholds

Document charitable intent and ensure no quid pro quo arrangements create complications

Documentation and Compliance (By December 31):

Ensure all year-end documentation is completed and filed

Verify corporation tax return deadline (12 months from year-end)

Confirm corporation tax payment deadline (9 months + 1 day from year-end)

File any outstanding R&D tax relief claims

Complete accounting records and reconcile ledger positions

Document all strategic tax decisions with clear rationale for HMRC audit defense

Frequently Asked Questions About Year-End Corporate Tax Planning

Q: What's the difference between year-end accounts and tax year for corporation tax purposes?

A: Your company's accounting year-end (when you close your books) and the tax year are independent. A company with a December 31 year-end files accounts for the year ending 31 December but the corporation tax is calculated on that 12-month period regardless of when the tax year changes. The key deadline is nine months and one day after your accounting year-end for payment.

Q: Can I still claim capital allowances if I haven't used my AIA in previous years?

A: The AIA is an annual allowance that resets each year; unused allowance doesn't carry forward. However, plant and machinery purchased but not relieved under AIA can still claim Writing-Down Allowance (WDA) at the main rate. Before April 2026, this rate is 18% per year; from April 2026, it reduces to 14%.

Q: Is a pension contribution or a dividend more tax-efficient for profit extraction?

A: For most companies, pension contributions offer superior tax efficiency because they reduce corporation tax, are exempt from income tax, and avoid National Insurance. However, pension contributions require a retirement commitment and have annual limits. For flexibility, a combination of pension contributions and dividends often provides optimal tax efficiency.

Q: How does marginal relief work if my company operates multiple entities?

A: The £50,000 and £250,000 profit thresholds for marginal relief are shared among all "associated companies" (companies with overlapping ownership). If you operate two companies each earning £75,000, they would each be treated as having £150,000 profit for marginal relief purposes, triggering higher effective rates.

Q: What documentation do I need for R&D tax relief claims?

A: HMRC requires detailed contemporaneous documentation showing: the research activities undertaken, the technical challenges encountered, the methodologies tested and why they failed, and how the project constitutes qualifying R&D. Project notes, emails, test logs, and technical decision records are essential. Lack of documentation is the primary reason for claim rejections.

Q: Can charitable donations be used to reduce profit below tax thresholds?

A: Yes, charitable donations are fully deductible. However, the donation must be genuinely motivated by charitable intent, not purely as a tax minimization strategy. If a donation is made solely to manipulate profit thresholds with no underlying charitable motivation, HMRC may challenge the deduction on the basis that it lacks a valid business purpose.

Q: When exactly must pension contributions be made to count as current-year business expenses?

A: For corporation tax purposes, the contribution must be paid into the pension scheme by the company's accounting year-end date. It doesn't matter when the contribution is actually paid by the scheme to the pension provider, as long as a binding commitment and payment arrangement exist by year-end.

Key Takeaways: Maximizing Your 2025 Tax Efficiency

Effective year-end corporate tax planning delivers substantial financial benefits beyond simple tax reduction. Strategic planning improves cash flow management, aligns business structure with operational reality, and positions your company for sustainable growth.

The core principles are straightforward: understand your profit position and tax bracket, leverage available reliefs comprehensively, time major decisions strategically around tax deadlines, and document all decisions thoroughly for HMRC compliance.

Capital allowances, loss relief mechanisms, pension contributions, and R&D tax credits represent billions of pounds in unclaimed relief across UK business annually. Many of these opportunities require year-end execution—once the tax year closes, many planning windows close permanently.

Your action now: Schedule a review of your financial position with your accounting advisor by December 15. Calculate your projected year-end profit, identify available tax planning opportunities specific to your business structure, and implement chosen strategies before December 31.

The difference between reactive tax compliance and proactive tax planning is substantially often worth tens of thousands of pounds annually for growing companies. This guide provides the foundation; working with a qualified tax advisor ensures your specific circumstances receive the attention they deserve.

About the author

Rudra Prakash Parida is a Financial Professional with an MBA in Business Administration and ACCA qualifications. He specialises in corporate tax planning, SME finance optimisation, and marketing analytics for growth-stage businesses. Through Growth Analytics Hub, he helps UK entrepreneurs and business owners unlock tax efficiency strategies and build data-driven growth systems.

Contact

Reach out for insights and support

Phone

+447768010239

© 2025. All rights reserved.