Financial Year-End: Make These 5 Critical Decisions Before Time Runs Out

Time-sensitive year-end tax decisions could save you £20K+. Master actionable strategies, deadline-critical tactics, and proven ROI before April 5, 2025.

FINANCE

Rudra Prakash Parida

11/19/202511 min read

Introduction: Your Last Window for Strategic Decisions Closes April 5, 2025

The clock is ticking. For UK business owners and decision-makers, the financial year-end deadline of 5 April 2026 marks the final opportunity to make strategic decisions that will directly impact your tax liability, cash flow, and profitability. Yet most businesses leave thousands of pounds on the table because they treat year-end as a compliance checkbox rather than a critical decision point.

Here's the reality: A business owner missing a single year-end deduction could lose £20,000 to £100,000+ in unnecessary tax payments. One real case involved a business that failed to accelerate equipment purchases before year-end and missed £28,000 in tax savings opportunities. Another business realized only after filing that they'd overlooked £85,000 in legitimate deductions, a £21,000 tax liability they could have avoided.

Decision #1: Accelerate Capital Asset Purchases Before April 5 (Deadline: URGENT)

1. The Tax Savings Opportunity: 100% Bonus Depreciation Is Available NOW

If your business needs equipment, machinery, vehicles, or technology infrastructure, the timing of your purchase is no longer academic it's a tax-saving lever worth thousands of pounds per transaction. The regulatory landscape has shifted in your favour, but the window is closing.

Key fact: Under the Annual Investment Allowance (AIA), businesses can claim up to 100% of qualifying capital expenditure as an immediate deduction if purchased and placed in service before 31 March 2026 (for corporation tax) or 5 April 2026 (for income tax). This allows you to write off the full cost against taxable profits immediately, rather than depreciating over years.

Real example: An S-corp ($2M+ revenue) considered various investments and decided to purchase £500,000 of qualifying plant and machinery before year-end. By accelerating the purchase and claiming 100% bonus depreciation, they deferred £500,000 of taxable income and saved approximately £150,000 in taxes in a single year.

2. What Qualifies and What Doesn't: Get This Right

Not every asset purchase qualifies. Only ask yourself these two questions:

Is it business property used in production? (Equipment, machinery, vehicles, technology systems, office fixtures that are integral to operations)

Is it a capital investment, not repairs or routine maintenance? (A new production machine qualifies; repair of an existing machine does not)

Key limitation: Real estate generally does NOT qualify for full AIA, though certain building elements may under specific conditions. If you're considering real estate investment, consult with your accountant immediately, the rules have nuances that directly affect your decision.

3. Your Action Steps: This Week

Audit your capital needs. What equipment, machinery, or technology upgrades have you deferred? What would improve operations next year?

Get quotes and commit. Purchase orders and deposits placed before 5 April lock in the tax year deduction.

Coordinate with your accountant. Confirm eligibility and proper classification to avoid HMRC challenges.

Urgency Tone: If you've been thinking about upgrading systems, purchasing delivery vehicles, or investing in production equipment, this decision has a 2-week deadline. Delaying to after April 5 means deferring tax benefits by an entire year, potentially costing you £50K+ in lost deductions if the investment is substantial.

Decision #2: Optimise Your Profit Extraction: Salary vs. Dividends vs. Pensions

1. The Real-World Problem: Most Owner-Managers Extract Profits Inefficiently

Most business owners leave £10,000 to £40,000 on the table annually through inefficient profit extraction. The gap exists because of complexity: balancing personal and corporate tax rates, National Insurance considerations, pension limits, and dividend allowance changes makes this deceptively complicated.

However, when you get it right, the savings are extraordinary. Here are three high-impact moves to evaluate immediately:

2. Strategy #1: Maximize Employee Bonuses Before Year-End

Deadline: Bonus paid by 31 March 2025 (for 2024/25 tax year deduction)

A bonus paid to yourself or employees before year-end is deductible in the current year, reducing corporate taxable profit. Employees then pay tax on the bonus in the year they receive it.

Financial impact: A director/owner who pays themselves a £50,000 bonus before year-end reduces their company's taxable profit by £50,000, saving approximately £12,500 in corporation tax (at 25% rate). The director pays personal income tax and National Insurance on the bonus, but the corporate tax saving often exceeds the personal tax cost, creating net tax savings.

Action: If you're comfortable taking additional income and your business has surplus profit, paying a year-end bonus is a classic tax decision with immediate ROI.

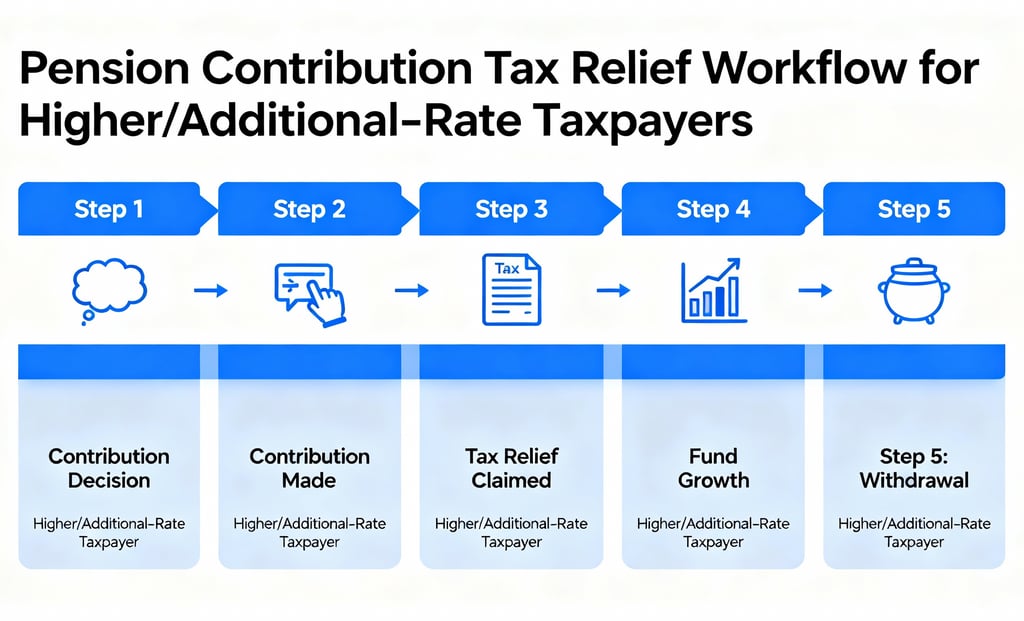

3. Strategy #2: Leverage Pension Contributions for Tax Relief at Your Marginal Rate

Deadline: Contribution made/declared by 31 March 2025 to claim current year relief

Most owner-managers underutilize pension contributions, not realizing they can contribute up to £60,000 annually and receive tax relief at their personal marginal rate.

Example: A higher-rate taxpayer (45% tax bracket) contributes £60,000 to their pension. They receive tax relief at 45%, meaning the contribution only costs them £33,000 in after-tax money. Compare this to dividend distributions (taxed at 39.35% for higher-rate taxpayers) and you see the compelling advantage.

Carry-forward provision: If you didn't max out contributions in prior years, you can carry forward unused allowances from the past three years, potentially allowing contributions up to £200,000 in a single year.

Action steps this week:

Check your pension contribution allowance (is it £60,000 or higher due to carry-forward?)

If you have accessible cash, a pension contribution is often the most tax-efficient profit extraction method

Confirm with your pension provider that contributions are received by 31 March 2025

4. Strategy #3: Reassess Your Dividend Timing and Structure

The dividend allowance just dropped from £1,000 to £500 this changes the math entirely.

If you've been taking most profits as dividends, reconsider. Higher-rate taxpayers now pay 39.35% tax on dividends over £500, whereas salary/bonus income is taxed at 45% but allows National Insurance savings and pension relief opportunities.

Critical decision: For your specific tax bracket and profit level, is salary, bonus, pension contribution, or dividend most efficient? The answer varies, but most owner-managed businesses benefit from a mixed approach: a modest salary (to secure National Insurance record), discretionary bonus as needed, pension contributions to max allowance, then dividends for remaining profit.

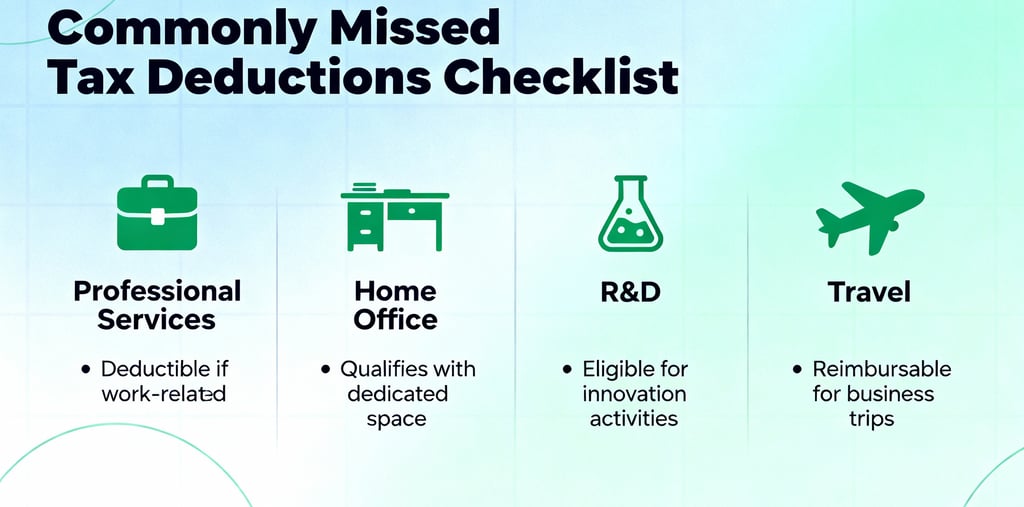

Decision #3: Claim Every Legitimate Business Deduction (You're Likely Missing Thousands)

The Data Reality: 45% of Tax Returns Contain Errors and many miss Deductions

45% of small business tax returns filed contain errors, and many involve missing or undervalued deductions. The average error results in additional tax liability exceeding £1,000. Yet these are completely preventable.

High-Probability Missed Deductions, Check Your Records Now

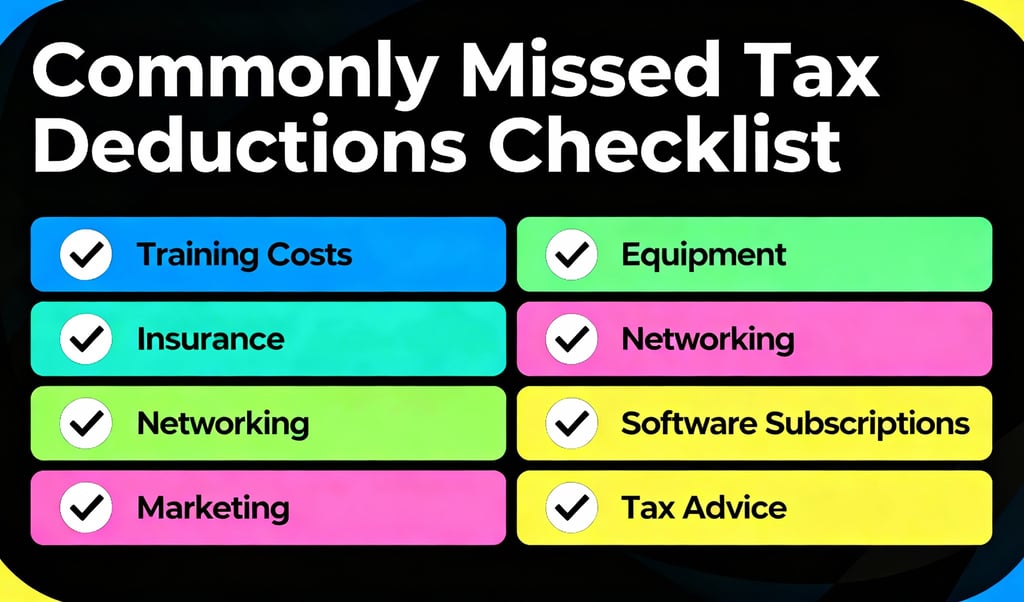

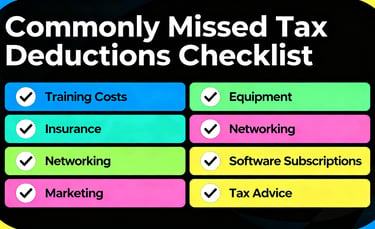

Professional services and subscriptions:

Accounting, bookkeeping, and tax advisory fees (fully deductible)

HR and payroll software subscriptions

Legal advice and contract review

Consulting services for business improvement

Professional membership fees

Home office and workspace:

Portion of rent/mortgage (if dedicated business space)

Utilities (apportioned to business use)

Office equipment and furniture

Internet and phone (business portion)

Research & Development and innovation:

R&D tax credits (potentially 19% of qualifying R&D spend).

Software development costs

Product testing and validation

Employee benefits and tax-efficient perks:

Pension contributions (both employer and employee matched)

Cycle-to-work schemes

Workplace health insurance

Training and professional development

Childcare vouchers (if still applicable)

Vehicle and travel:

Mileage (45p per business mile under HMRC rates)

Fuel and maintenance

Parking and tolls

Client entertainment (subject to limits)

Key action: Review your records for December 2024 through March 2025. Are there invoices you've paid but not claimed as deductions? Expenses you categorized as personal that have business elements?

The Cost of Missing Deductions: Real Numbers

One business owner realized in April (after filing) that they'd failed to claim £12,000 in legitimate home office expenses over three years resulting in £3,000 of unnecessary tax payments. Another owner missed quarterly software subscriptions totalling £8,000 annually a £2,000 annual tax liability they could have avoided.

Decision #4: Make Critical Timing Decisions on Income and Expenses

Should You Defer Income or Accelerate Expenses? Make This Decision Now

If you're approaching higher tax brackets or expecting income volatility, timing decisions matter enormously.

Income deferral strategy: If you expect this year's income to push you into a higher tax bracket, consider delaying invoicing of projects until after 5 April 2026. This defers the income to the next tax year, keeping your current-year income lower and potentially avoiding higher tax rates.

Real scenario: A freelance consultant invoiced £150,000 in January-February. Realizing they'd hit the higher-rate threshold, they negotiated with clients to defer final invoices until early April 2025 deferring approximately £30,000 of income to the next tax year and saving approximately £9,000 in tax (assuming 30% marginal rate).

Expense acceleration strategy: Conversely, if you have discretionary expenses scheduled for April, consider pulling them into March. Bonus payments, equipment purchases, and professional services booked in the current year are deductible now rather than next year.

Decision #5: Explore Specific Tax Reliefs Before the Window Closes

Business Asset Disposal Relief (BADR): Current 10% Rate Ends Soon

If you're planning to sell shares or business assets, the timing is critical. Business Asset Disposal Relief currently allows you to pay Capital Gains Tax at just 10% on qualifying disposals compared to the standard 20% rate.

Real financial impact: A business owner selling shares for a £500,000 gain:

Under BADR (10% rate): £50,000 tax liability

Under standard CGT (20% rate): £100,000 tax liability

Potential saving: £50,000

The catch: You must meet specific conditions, and disposals must occur before 5 April 2026 to qualify under current rates.

Action: If you're considering asset disposals, speak with your accountant immediately. BADR eligibility has specific holding periods and conditions to get professional confirmation before committing.

Annual ISA and Tax-Free Investment Allowances

If you have surplus cash, maximizing tax-free savings vehicles before 5 April 2026 is a no-brainer decision:

Individual Savings Accounts (ISAs): You can invest up to £20,000 per tax year in tax-free savings

Junior ISAs: Invest up to £9,000 per child for tax-free growth

This isn't exciting, but it's unambiguous tax optimization: money invested in ISAs before 5 April generates tax-free returns indefinitely, while the same money in standard savings accounts is taxed at your marginal rate.

Real-World Case Study: From Missed Opportunity to £42K Tax Savings

The Scenario:

A mid-sized professional services firm (£3.2M revenue, 8 staff) approached year-end assuming they'd break even tax-wise. However, their accountant conducted a strategic year-end review discovering:

Deferred equipment purchase: The firm needed new workstations and software. By purchasing before year-end rather than in April, they claimed £45,000 in capital allowances (saving £11,250 in corporation tax)

Underutilized pension allowance: The owner-manager had available carry-forward pension allowance of £120,000 (three years unused). Maximizing the contribution (£120,000) at their 45% marginal rate created £54,000 in tax relief

Missed professional service deductions: The firm had paid £8,000 in HR consulting but not classified it as deductible. Once properly recorded, it reduced taxable profit by £8,000 (saving £2,000 in taxes)

Discretionary bonus strategy: The owner paid themselves a £30,000 performance bonus before year-end, reducing company taxable profit by £30,000 (saving £7,500 in corporation tax)

Home office optimization: Allocating home office expenses (utilities, internet, portion of rent) that hadn't been claimed previously added another £3,000 in deductions (saving £750 in taxes)

Total tax savings identified: £42,500

Most critically: Without the year-end strategic review, the business would have filed their tax return leaving these opportunities unclaimed writing an unnecessary £42,500 cheque to HMRC.

The Cost of Inaction: What Happens If You Don't Decide

If you delay these decisions past 5 April 2026, the consequences are real:

Capital purchases made in April 2026 are deductible for the 2026/27 tax year a full year delayed, deferring tax benefits and wasting cash flow

Bonuses paid after year-end don't reduce current year corporate tax, meaning if you had £100K surplus profit you're paying tax on all of it rather than extracting via bonus first

Missed deductions can't be amended once returns are filed, leaving taxpayers overpaying for years until discovered

Income deferral opportunities close on 5 April you can't retroactively shift invoicing dates

Tax reliefs with specific deadlines expire, and there's no second chance with HMRC

The bottom line: Every day past mid-March 2026 that you haven't finalised these decisions is a day you're leaving money on the table.

Action Plan: Your Week-by-Week Year-End Checklist

1. Week of March 17–21, 2026 (URGENT: NOW)

Schedule call with your accountant to discuss your specific situation, tax liability projection, and opportunities

Audit capital asset needs: What equipment/tech do you need? Get quotes and confirm viability

Review your profit extraction strategy: Assess bonus, pension, and dividend timing for your specific tax bracket

Compile a comprehensive deductions list: Go through bank statements and invoices to capture every business expense

2. Week of March 24–28, 2027

Commit to capital purchases: Issue purchase orders for any equipment acquisitions to lock in current-year deduction

Finalize bonus and compensation decisions: Confirm amounts and beneficiaries; schedule payments before 31 March

Execute pension contributions: If maximizing allowance, ensure contributions are made/declared by 31 March

Review income projections: Determine if deferring any income to next tax year is strategically beneficial

Week of March 31–April 4, 2026 (FINAL WINDOW)

Process final transactions: Ensure bonuses, equipment payments, and last-minute deductible expenses are recorded in current tax year

Prepare all documentation: Gather receipts, invoices, and supporting evidence for your accountant

Final review with accountant: Confirm tax position, filing deadlines, and next steps

After April 5, 2025

File accounts and tax returns by required deadline (9 months after year-end for companies; 31 January for self-employed)

Make any outstanding tax payments to avoid penalties

Begin next year's planning: Use this year's actual performance to inform next year's strategy

Addressing Your Key Questions: FAQ

Q1: My accountant hasn't reached out about year-end planning. Should I be concerned?

A: Yes. Proactive accountants initiate year-end strategy discussions in January and February. If you haven't heard from yours by late February, contact them directly. If they're unresponsive, this is a sign to consider switching providers. Year-end tax planning isn't optional it's where accountants deliver the most direct value.

Q2: What if I don't have a lot of cash available for capital purchases or pension contributions?

A: Focus on the decisions that don't require cash outlay: ensure you're claiming every deductible expense, assess whether income deferral is beneficial, and confirm your profit extraction method (bonus vs. dividend) is optimized for your tax bracket. These require no additional cash investment and still deliver significant savings.

Q3: Is it too late if we're already in late March?

A: Absolutely not. You still have until 5 April to make critical decisions. Bonuses can be authorized and paid within days. Equipment purchases can be finalized with urgent delivery. Pension contributions can be made electronically. It's tight, but you have options.

Q4: What happens if I miss a deadline?

A: It depends on the deadline. Missing the 31 March deadline for bonus deduction means you lose the deduction for this year (though the bonus itself is still paid). Missing the 5 April date for capital purchases means the deduction transfers to the next tax year. Missing the income tax filing deadline results in penalties ranging from £100 to several thousand pounds. Plan to meet deadlines; don't rely on late filing forgiveness.

Q5: Should I make these decisions on my own or with professional help?

A: Get professional advice. The value of an accountant identifying £20K–£50K in tax savings far exceeds the cost of consultation. Tax law is complex, and mistakes are costly. For owner-managed businesses, a strategic consultation with your accountant before 31 March is one of the highest-ROI investments you can make.

Stop leaving thousands on the table. These decisions close on 5 April 2026 period.

You've now seen the specific moves, the real numbers, and the cost of inaction. The question isn't whether year-end tax optimization matters, it's whether you'll seize this final window or watch the deadline pass.

Book your year-end strategy session TODAY. Our tax specialists will:

Project your final tax liability and identify specific savings opportunities

Confirm which capital purchases and timing decisions deliver maximum ROI

Optimize your profit extraction method for your specific tax bracket and personal situation

Create a definitive action plan with clear next steps

About the author

Rudra Prakash Parida is a Financial Professional with an MBA in Business Administration and ACCA qualifications. He specialises in corporate tax planning, SME finance optimisation, and marketing analytics for growth-stage businesses. Through Growth Analytics Hub, he helps UK entrepreneurs and business owners unlock tax efficiency strategies and build data-driven growth systems.

A 90-minute strategic consultation typically identifies £15K–£50K in tax savings.

Enquiry: services@growthanalytica.co.uk

Contact

Reach out for insights and support

Phone

+447768010239

© 2025. All rights reserved.